- Strong execution of operating plans

- Solid cost & capital management

- Ramp-up of Grasberg underground advancing on schedule

- Fourth-quarter 2020 copper and gold sales 3% and 9% above October 2020 estimates

- Strong cash flow generation

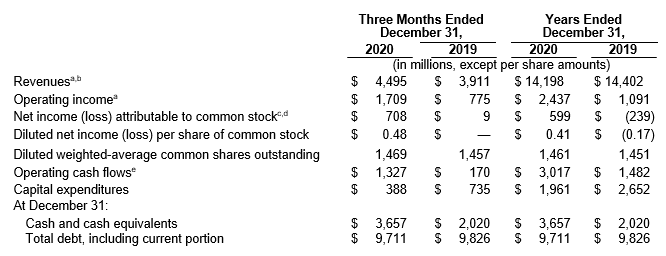

- Net income attributable to common stock totaled $708 million, $0.48 per share, in fourth-quarter 2020. After adjusting for net credits totaling $142 million, $0.10 per share, fourth-quarter 2020 adjusted net income attributable to common stock totaled $566 million, or $0.39 per share.

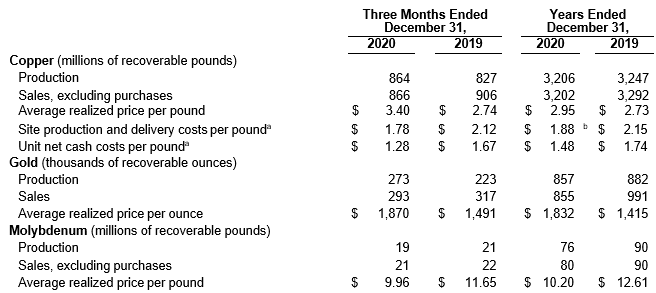

- Consolidated sales totaled 866 million pounds of copper, 293 thousand ounces of gold and 21 million pounds of molybdenum in fourth-quarter 2020, and 3.2 billion pounds of copper, 855 thousand ounces of gold and 80 million pounds of molybdenum for the year 2020. Consolidated sales for the year 2021 are expected to approximate 3.8 billion pounds of copper, 1.3 million ounces of gold and 85 million pounds of molybdenum, including 825 million pounds of copper, 275 thousand ounces of gold and 20 million pounds of molybdenum in first-quarter 2021.

- Average realized prices in fourth-quarter 2020 were $3.40 per pound for copper, $1,870 per ounce for gold and $9.96 per pound for molybdenum.

- Average unit net cash costs in fourth-quarter 2020 were $1.28 per pound of copper and $1.48 per pound of copper for the year 2020. Unit net cash costs are expected to average $1.25 per pound of copper for the year 2021.

- Operating cash flows totaled $1.3 billion (including $0.3 billion from working capital and other sources) in fourth-quarter 2020 and $3.0 billion (including $0.7 billion from working capital and other sources) for the year 2020. Based on current sales volume and cost estimates, and assuming average prices of $3.50 per pound for copper, $1,850 per ounce for gold and $9.00 per pound for molybdenum, operating cash flows are expected to approximate $5.5 billion (including $0.4 billion from working capital and other sources) for the year 2021.

- Capital expenditures totaled $0.4 billion (including approximately $0.3 billion for major projects) in fourth-quarter 2020 and $2.0 billion (including approximately $1.2 billion for major projects) for the year 2020. Capital expenditures for the year 2021 are expected to approximate $2.3 billion, including $1.4 billion for major projects primarily associated with underground development activities in the Grasberg minerals district in Indonesia.

- During fourth-quarter 2020, FCX sold an undeveloped exploration project in the Democratic Republic of Congo (DRC) for $550 million and recognized an after-tax gain of $350 million. After-tax net cash proceeds to FCX totaled $415 million.

- At December 31, 2020, consolidated debt totaled $9.7 billion and consolidated cash totaled $3.7 billion. FCX had no borrowings and $3.5 billion available under its revolving credit facility at December 31, 2020.

PHOENIX, AZ, January 26, 2021 – Freeport-McMoRan Inc. (NYSE: FCX) reported net income attributable to common stock of $708 million, $0.48 per share, in fourth-quarter 2020 and $599 million, $0.41 per share, for the year 2020. After adjusting for net credits totaling $142 million, $0.10 per share, mostly associated with a gain on sale of assets, partly offset by charges for a litigation settlement and international tax matters, and other net charges, adjusted net income attributable to common stock totaled $566 million, $0.39 per share, in fourth-quarter 2020. For additional information, refer to the supplemental schedule, “Adjusted Net Income,” on page VII.

Richard C. Adkerson, President and Chief Executive Officer, said, “During 2020, our global team responded to the challenges of the pandemic in an exceptional fashion, safeguarding our people, communities and assets as we executed and delivered on our clearly defined strategy. Together we achieved strong operating performance and project execution, establishing a solid foundation for future growth in sales volumes and cash flows. We are enthusiastic about the future prospects for our business based on the positive outlook for the markets we serve, our long-lived and high-quality copper assets, our seasoned and highly motivated global organization and the critical role of copper to the technologies necessary to deliver clean energy and support the global transition to a low-carbon economy.”

SUMMARY FINANCIAL DATA

- For segment financial results, refer to the supplemental schedules, “Business Segments,” beginning on page X.

- Includes favorable (unfavorable) adjustments to prior period provisionally priced concentrate and cathode copper sales totaling $113 million ($41 million to net income attributable to common stock or $0.03 per share) in fourth-quarter 2020, $33 million ($14 million to net income attributable to common stock or $0.01 per share) in fourth-quarter 2019, $(102) million ($(42) million to net income attributable to common stock or $(0.03) per share) for the year 2020 and $58 million ($24 million to net loss attributable to common stock or $0.02 per share) for the year 2019. For further discussion, refer to the supplemental schedule, “Derivative Instruments,” beginning on page IX.

- Includes net credits (charges) totaling $142 million ($0.10 per share) in fourth-quarter 2020, $(22) million ($(0.02) per share) in fourth-quarter 2019, $(191) million ($(0.13) per share) for the year 2020 and $(275) million ($(0.19) per share) for the year 2019 that are described in the supplemental schedule, “Adjusted Net Income,” beginning on page VII.

- FCX defers recognizing profits on intercompany sales until final sales to third parties occur. For a summary of net impacts from changes in these deferrals, refer to the supplemental schedule, “Deferred Profits,” on page X.

- Working capital and other sources totaled $346 million in fourth-quarter 2020, $75 million in fourth-quarter 2019, $665 million for the year 2020 and $349 million for the year 2019.

SUMMARY OPERATING DATA

- Reflects per pound weighted-average production and delivery costs and unit net cash costs (net of by-product credits) for all copper mines, before net noncash and other costs. For reconciliations of per pound unit costs by operating division to production and delivery costs applicable to sales reported in FCX’s consolidated financial statements, refer to the supplemental schedules, “Product Revenues and Production Costs,” beginning on page XIII.

- Excludes charges totaling $0.06 per pound of copper associated with the COVID-19 pandemic and our April 2020 revised operating plans.

Consolidated Sales Volumes

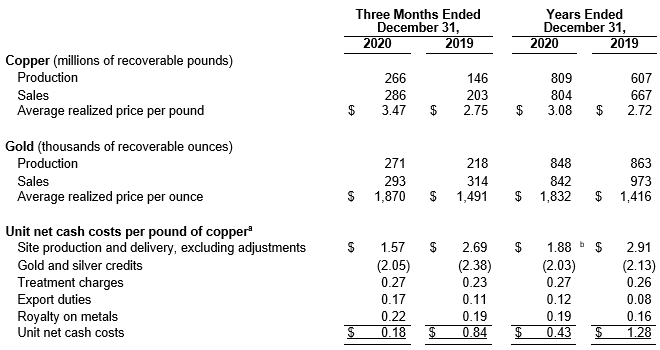

Fourth-quarter 2020 copper sales of 866 million pounds were 3 percent higher than the October 2020 estimate of 840 million pounds of copper, primarily reflecting higher sales from Cerro Verde and Indonesia. Fourth- quarter 2020 copper sales were lower than fourth-quarter 2019 sales of 906 million pounds of copper, primarily reflecting previously announced operating plan adjustments, partly offset by higher mining rates and copper ore grades in Indonesia.

Fourth-quarter 2020 gold sales of 293 thousand ounces were 9 percent higher than the October 2020 estimate of 270 thousand ounces of gold, primarily reflecting higher gold ore grades in Indonesia. Fourth-quarter 2020 gold sales were lower than fourth-quarter 2019 sales of 317 thousand ounces of gold, primarily reflecting timing of shipments in fourth-quarter 2019.

Fourth-quarter 2020 molybdenum sales of 21 million pounds were in line with both the October 2020 estimate and fourth-quarter 2019 sales of 22 million pounds.

Consolidated sales volumes for the year 2021 are expected to approximate 3.8 billion pounds of copper, 1.3 million ounces of gold and 85 million pounds of molybdenum, including 825 million pounds of copper, 275 thousand ounces of gold and 20 million pounds of molybdenum in first-quarter 2021. Projected sales volumes are dependent on operational performance, continued progress of the ramp-up of underground mining at PT Freeport Indonesia (PT-FI), impacts and duration of the COVID-19 pandemic, timing of shipments, and other factors.

Consolidated Unit Net Cash Costs

Consolidated average unit net cash costs (net of by-product credits) for FCX’s copper mines of $1.28 per pound of copper in fourth-quarter 2020, were lower than the October 2020 estimate of $1.32 per pound, primarily reflecting higher copper sales volumes and by-product credits. As anticipated, consolidated average unit net cash costs in fourth-quarter 2020 of $1.28 per pound were significantly lower than the fourth-quarter 2019 average of

$1.67 per pound, primarily reflecting lower mining costs and higher by-product credits.

Assuming average prices of $1,850 per ounce of gold and $9.00 per pound of molybdenum for 2021 and achievement of current sales volume and cost estimates, consolidated unit net cash costs (net of by-product credits) for FCX’s copper mines are expected to average $1.25 per pound of copper for the year 2021. The impact of price changes on 2021 consolidated unit net cash costs would approximate $0.03 per pound of copper for each $100 per ounce change in the average price of gold and $0.01 per pound of copper for each $2 per pound change in the average price of molybdenum. Quarterly unit net cash costs vary with fluctuations in sales volumes and realized prices, primarily for gold and molybdenum.

MINING OPERATIONS

North America Copper Mines. FCX operates seven open-pit copper mines in North America – Morenci, Bagdad, Safford (including Lone Star), Sierrita and Miami in Arizona, and Chino and Tyrone in New Mexico. In addition to copper, certain of these mines produce molybdenum concentrate, gold and silver. All of the North America mining operations are wholly owned, except for Morenci. FCX records its 72 percent undivided joint venture interest in Morenci using the proportionate consolidation method.

Operating and Development Activities. FCX’s North America operating sites continue to focus on strong execution of operating plans. Production from Lone Star continues to ramp-up on schedule and is expected to exceed 200 million pounds of copper for the year 2021. FCX plans to advance studies for potential expansions and long-term development options for its large-scale sulfide resources at Lone Star.

In January 2021, FCX restarted mining activities at the Chino mine at a reduced rate of approximately 100 million pounds of copper per year (approximately 50 percent of capacity).

FCX has substantial resources in the United States (U.S.), primarily associated with existing mining operations, and will continue to assess options for future growth.

Operating Data. Following is summary consolidated operating data for the North America copper mines:

- Includes reductions to average realized prices of $0.02 per pound of copper for the year 2020 related to forward sales contracts covering 150 million pounds of copper sales for May and June 2020 at a fixed price of $2.34 per pound. There are no remaining forward sales contracts.

- Refer to summary operating data on page 3 for FCX’s consolidated molybdenum sales, which includes sales of molybdenum produced at the North America copper mines.

- For a reconciliation of unit net cash costs per pound to production and delivery costs applicable to sales reported in FCX’s consolidated financial statements, refer to the supplemental schedules, “Product Revenues and Production Costs,” beginning on page XIII.

- Excludes charges totaling $0.02 per pound of copper primarily associated with the April 2020 revised operating plans (including employee separation costs) and the COVID-19 pandemic (including health and safety costs).

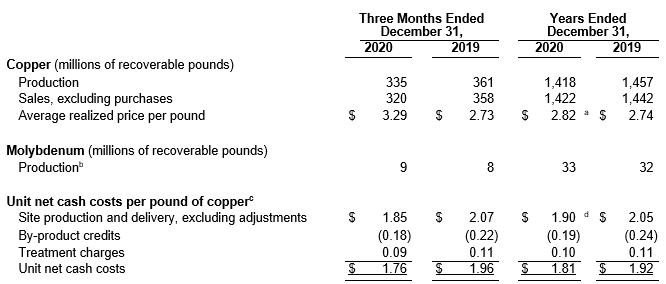

FCX’s consolidated copper sales volumes from North America of 320 million pounds in fourth-quarter 2020 were lower than fourth-quarter 2019 copper sales volumes of 358 million pounds, primarily reflecting lower mining rates associated with the April 2020 revised operating plans, partly offset by production from Lone Star. North America copper sales are estimated to approximate 1.5 billion pounds for the year 2021, compared with 1.4 billion pounds for the year 2020.

Average unit net cash costs (net of by-product credits) for the North America copper mines of $1.76 per pound of copper in fourth-quarter 2020 were lower than fourth-quarter 2019 unit net cash costs of $1.96 per pound, primarily reflecting lower mining rates and cost reductions associated with the April 2020 revised operating plans, partly offset by lower sales volumes.

Average unit net cash costs (net of by-product credits) for the North America copper mines are expected to approximate $1.86 per pound of copper for the year 2021, based on achievement of current sales volume and cost estimates and assuming an average molybdenum price of $9.00 per pound. North America’s average unit net cash costs for the year 2021 would change by approximately $0.05 per pound of copper for each $2 per pound change in the average price of molybdenum.

South America Mining. FCX operates two copper mines in South America – Cerro Verde in Peru (in which FCX owns a 53.56 percent interest) and El Abra in Chile (in which FCX owns a 51 percent interest). These operations are consolidated in FCX’s financial statements. In addition to copper, the Cerro Verde mine produces molybdenum concentrate and silver.

Operating and Development Activities. During fourth-quarter 2020, Cerro Verde continued to increase milling rates to an average of 373,200 metric tons of ore per day while operating consistent with the April 2020 revised operating plans and under strict COVID-19 restrictions and protocols. FCX expects Cerro Verde’s mill rates to average approximately 360,000 metric tons of ore per day in 2021 with the potential to ramp-up to pre-COVID-19 levels approximating 400,000 metric tons of ore per day as COVID-19 restrictions are lifted.

El Abra plans to increase operating rates during 2021 to pre-COVID-19 levels, subject to ongoing monitoring of public health conditions in Chile. Incremental copper production associated with increasing El Abra’s stacking rates from 65,000 metric tons of ore per day to over 100,000 metric tons of ore per day, approximates 70 million pounds per year beginning in 2022.

FCX continues to evaluate a large-scale expansion at El Abra to process additional sulfide material and to achieve higher recoveries. El Abra’s large sulfide resource could potentially support a major mill project similar to facilities constructed at Cerro Verde. Technical and economic studies continue to be evaluated to determine the optimal scope and timing for the project in parallel with extending the life of the current leaching operation.

Operating Data. Following is summary consolidated operating data for South America mining:

- Refer to summary operating data on page 3 for FCX’s consolidated molybdenum sales, which includes sales of molybdenum produced at Cerro Verde.

- For a reconciliation of unit net cash costs per pound to production and delivery costs applicable to sales reported in FCX’s consolidated financial statements, refer to the supplemental schedules, “Product Revenues and Production Costs,” beginning on page XIII.

- Excludes charges totaling $0.09 per pound of copper, primarily associated with idle facility (Cerro Verde) and contract cancellation costs related to the COVID-19 pandemic, and employee separation costs associated with the April 2020 revised operating plans.

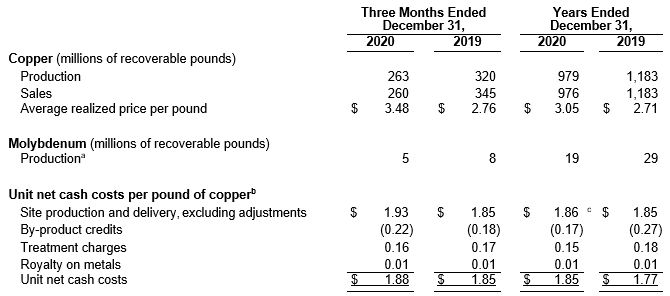

FCX’s consolidated copper sales volumes from South America of 260 million pounds in fourth-quarter 2020 were lower than fourth-quarter 2019 copper sales volumes of 345 million pounds, primarily reflecting lower mining rates associated with COVID-19 protocols and the April 2020 revised operating plans.

Copper sales from South America mining are expected to approximate 1.0 billion pounds for the year 2021, consistent with the year 2020.

Average unit net cash costs (net of by-product credits) for South America mining of $1.88 per pound of copper in fourth-quarter 2020 were higher than average unit net cash costs of $1.85 per pound in fourth-quarter 2019, primarily reflecting lower sales volumes, mostly offset by lower mining and input costs and higher by-product credits.

Average unit net cash costs (net of by-product credits) for South America mining are expected to approximate $1.92 per pound of copper for the year 2021, based on current sales volume and cost estimates and assuming an average price of $9.00 per pound of molybdenum.

Indonesia Mining. PT-FI operates one of the world’s largest copper and gold mines at the Grasberg minerals district in Papua, Indonesia. PT-FI produces copper concentrate that contains significant quantities of gold and silver. FCX has a 48.76 percent ownership interest in PT-FI and manages its mining operations. Under the terms of the shareholders agreement, FCX’s economic interest in PT-FI approximates 81 percent through 2022. PT-FI’s results are consolidated in FCX’s financial statements.

Operating and Development Activities. The ramp-up of underground production at the Grasberg minerals district in Indonesia continues to advance on schedule. During fourth-quarter 2020, a total of 56 new drawbells were constructed at the Grasberg Block Cave and Deep Mill Level Zone (DMLZ) underground mines, bringing cumulative open drawbells to over 370. Combined average production from the Grasberg Block Cave and DMLZ mines approximated 85,000 metric tons of ore per day during fourth-quarter 2020 (including approximately 95,000 metric tons of ore per day during the month of December). PT-FI expects production for the year 2021 to approximate 1.4 billion pounds of copper and 1.4 million ounces of gold, which is nearly double 2020 levels.

The successful completion of this ramp up is expected to enable PT-FI to generate average annual production for the next several years of 1.55 billion pounds of copper and 1.6 million ounces of gold at an attractive unit net cash cost, providing significant margins and cash flows.

PT-FI’s estimated annual capital spending on underground mine development projects is expected to average approximately $0.9 billion per year for the two-year period 2021 through 2022, net of scheduled contributions from PT Indonesia Asahan Aluminium (Persero) (PT Inalum). In accordance with applicable accounting guidance, aggregate costs (before scheduled contributions from PT Inalum), which are expected to average $1.1 billion per year for the two-year period 2021 through 2022, will be reflected as an investing activity in FCX’s cash flow statement, and contributions from PT Inalum will be reflected as a financing activity.

Indonesia Smelter. As a result of COVID-19 mitigation measures, there have been disruptions to work and travel schedules of international contractors and restrictions on access to the proposed physical site of the new smelter in Gresik, Indonesia. Accordingly, during 2020, PT-FI notified the Indonesia government of delays in achieving the completion timeline of December 2023. PT-FI continues to discuss with the Indonesia government a deferred schedule for the project as well as other alternatives in light of the ongoing COVID-19 pandemic and volatile global economic conditions.

In connection with its commitment to develop additional smelter capacity in Indonesia, PT-FI has advanced discussions with the majority owner of the existing smelter in Gresik, Indonesia (PT Smelting), which is 25-percent owned by PT-FI, regarding an expansion of the smelter to increase smelter concentrate treatment capacity by approximately 30 percent (300,000 metric tons of concentrate per year). Commercial and financial arrangements for this potential project are being advanced.

An expansion of PT Smelting would reduce PT-FI’s smelter development commitment from 2.0 million metric tons of concentrate per year to 1.7 million metric tons per year. PT-FI continues to evaluate a new greenfield smelter project located in East Java in parallel with discussions with a third party to develop new smelter capacity at an alternate location in partnership with PT-FI.

Operating Data. Following is summary consolidated operating data for Indonesia mining:

- For a reconciliation of unit net cash costs per pound to production and delivery costs applicable to sales reported in FCX’s consolidated financial statements, refer to the supplemental schedules, “Product Revenues and Production Costs,” beginning on page XIII.

- Excludes COVID-19 related costs (including one-time incremental employee benefits and health and safety costs) totaling $0.02 per pound of copper.

FCX’s consolidated copper sales from PT-FI of 286 million pounds in fourth-quarter 2020 were higher than fourth-quarter 2019 consolidated copper sales of 203 million pounds, primarily reflecting higher mining rates and copper ore grades. FCX’s consolidated gold sales from PT-FI of 293 thousand ounces in fourth-quarter 2020 were lower than fourth-quarter 2019 consolidated gold sales of 314 thousand ounces, primarily reflecting timing of shipments in fourth-quarter 2019.

FCX’s consolidated sales volumes from PT-FI are expected to approximate 1.3 billion pounds of copper and

1.3 million ounces of gold for the year 2021, compared with 804 million pounds of copper and 0.8 million ounces of gold in 2020.

Because of the fixed nature of a large portion of PT-FI’s costs, unit net cash costs can vary significantly from quarter to quarter depending on copper and gold volumes. PT-FI’s unit net cash costs (net of gold and silver credits) of $0.18 per pound of copper in fourth-quarter 2020, were lower than unit net cash costs of $0.84 per pound in fourth-quarter 2019, primarily reflecting higher copper sales volumes and lower mining costs, partly offset by the lower gold and silver credits.

Average unit net cash costs (net of gold and silver credits) for PT-FI are expected to approximate $0.06 per pound of copper for the year 2021, based on achievement of current sales volume and cost estimates and assuming an average gold price of $1,850 per ounce. PT-FI’s average unit net cash costs for the year 2021 would change by approximately $0.09 per pound of copper for each $100 per ounce change in the average price of gold.

Molybdenum Mines. FCX operates two wholly owned molybdenum mines in Colorado – the Henderson underground mine and the Climax open-pit mine. The Henderson and Climax mines produce high-purity, chemical- grade molybdenum concentrate, which is typically further processed into value-added molybdenum chemical products. The majority of the molybdenum concentrate produced at the Henderson and Climax mines, as well as from FCX’s North America and South America copper mines, is processed at FCX’s conversion facilities.

Operating and Development Activities. Production from the molybdenum mines of 5 million pounds of molybdenum in fourth-quarter 2020 approximated fourth-quarter 2019. Refer to summary operating data on page 3 for FCX’s consolidated molybdenum sales and average realized prices, which includes sales of molybdenum produced at the Molybdenum mines and from FCX’s North America and South America copper mines.

Average unit net cash costs for the Molybdenum mines of $9.23 per pound of molybdenum in fourth-quarter 2020 were lower than average unit net cash costs of $14.20 per pound in fourth-quarter 2019, primarily reflecting lower mining and input costs associated with the April 2020 revised operating plans. Based on current sales volume and cost estimates, average unit net cash costs for the Molybdenum mines are expected to approximate $9.80 per pound of molybdenum for the year 2021.

For a reconciliation of unit net cash costs per pound to production and delivery costs applicable to sales reported in FCX’s consolidated financial statements, refer to the supplemental schedules, “Product Revenues and Production Costs,” beginning on page XIII.

EXPLORATION

FCX’s mining exploration activities are generally associated with its existing mines, focusing on opportunities to expand reserves and resources to support development of additional future production capacity. Exploration results continue to indicate opportunities for significant future potential reserve additions in North America and South America. Exploration expenditures for the year 2021 are expected to approximate $34 million, consistent with the year 2020. FCX has long-lived reserves and a significant resource position in its existing portfolio.

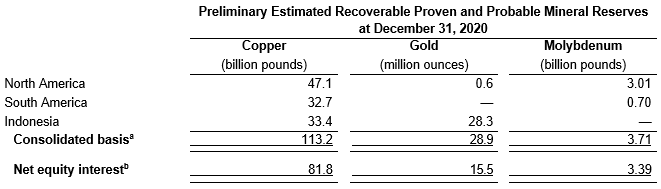

PRELIMINARY ESTIMATED RECOVERABLE PROVEN AND PROBABLE MINERAL RESERVES

FCX has significant reserves, resources and future development opportunities within its portfolio of mining assets. FCX’s preliminary estimated consolidated recoverable proven and probable reserves from its mines at

December 31, 2020, include 113.2 billion pounds of copper, 28.9 million ounces of gold and 3.71 billion pounds of molybdenum, which were determined using metal price assumptions of $2.50 per pound for copper, $1,200 per ounce for gold and $10.00 per pound for molybdenum. The preliminary estimated recoverable proven and probable mining reserves presented in the table below represent the estimated metal quantities from which FCX expects to be paid after application of estimated metallurgical recovery rates and smelter recovery rates, where applicable.

Recoverable reserve volumes are those which FCX estimates can be economically and legally extracted or produced at the time of the reserve determination.

- Consolidated reserves represent estimated metal quantities after reduction for FCX’s joint venture partner interest at the Morenci mine in North America. Excluded from the table above are FCX’s estimated recoverable proven and probable reserves of 362 million ounces of silver, which were determined using $15 per ounce.

- Net equity interest reserves represent estimated consolidated metal quantities further reduced for noncontrolling interest ownership. FCX’s net equity interest for estimated metal quantities in Indonesia reflects 81.27 percent through 2022 and 48.76 percent from 2023 through 2041. Excluded from the table above are FCX’s estimated net recoverable proven and probable reserves of 247 million ounces of silver.

The following table summarizes changes in FCX’s preliminary estimated consolidated recoverable proven and probable copper, gold and molybdenum reserves during 2020:

In addition to the preliminary estimated consolidated recoverable proven and probable reserves, FCX’s preliminary estimated mineralized material at December 31, 2020, which was assessed using $3.00 per pound for copper, totaled 120 billion pounds of incremental contained copper. FCX continues to pursue opportunities to convert this material into reserves, future production volumes and cash flow.

CASH FLOWS, CASH AND DEBT

Operating Cash Flows. FCX generated operating cash flows of $1.3 billion (including $0.3 billion from working capital and other sources) in fourth-quarter 2020 and $3.0 billion (including $0.7 billion from working capital and other sources) for the year 2020.

Based on current sales volume and cost estimates, and assuming average prices of $3.50 per pound of copper, $1,850 per ounce of gold and $9.00 per pound of molybdenum, FCX’s consolidated operating cash flows are estimated to approximate $5.5 billion (including $0.4 billion from working capital and other sources) for the year 2021. The impact of price changes during 2021 on operating cash flows would approximate $380 million for each

$0.10 per pound change in the average price of copper, $120 million for each $100 per ounce change in the average price of gold and $80 million for each $2 per pound change in the average price of molybdenum.

Capital Expenditures. Capital expenditures totaled $0.4 billion in fourth-quarter 2020 (including approximately $0.3 billion primarily associated with underground development activities in the Grasberg minerals district) and $2.0 billion for the year 2020 (including approximately $1.2 billion primarily associated with underground development activities in the Grasberg minerals district and the now completed Lone Star copper leach project).

Capital expenditures are expected to approximate $2.3 billion for the year 2021, including $1.4 billion for major projects primarily associated with underground development activities in the Grasberg minerals district.

Asset Sale. On December 11, 2020, FCX completed the sale of its interests in the Kisanfu undeveloped exploration project in the DRC for $550 million (after-tax net cash proceeds totaled $415 million). An after-tax gain of

$350 million was recorded in fourth-quarter 2020.

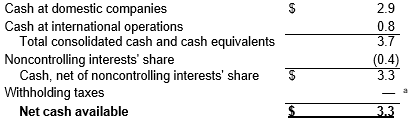

Cash. Following is a summary of the U.S. and international components of consolidated cash and cash equivalents available to the parent company, net of noncontrolling interests’ share, taxes and other costs at December 31, 2020 (in billions):

a. Rounds to less than $0.1 billion.

Debt. Following is a summary of total debt and the weighted-average interest rates at December 31, 2020 (in millions, except percentages).

In December 2020, Cerro Verde prepaid $305 million of its credit facility that was scheduled to mature in December 2021 and recorded a $1 million loss on early extinguishment of debt. The remaining balance matures in June 2022.

At December 31, 2020, FCX had no borrowings, $10 million in letters of credit issued and $3.5 billion available under its revolving credit facility. FCX has no senior note maturities until 2022.

FINANCIAL POLICY

FCX’s financial policy will continue to prioritize liquidity and balance sheet management during this period of global economic uncertainty associated with the ongoing COVID-19 pandemic. With continued strong financial performance and successful execution of FCX’s operating plans, management expects to recommend to the Board of Directors (Board) the resumption of common stock dividends during 2021 and anticipates an ongoing ability to increase cash returns to shareholders in the future. The declaration and payment of future dividends is at the discretion of the Board and will be assessed on an ongoing basis, taking into account FCX’s financial results, cash requirements, future prospects, global economic conditions, and other factors deemed relevant by the Board.

WEBCAST INFORMATION

A conference call with securities analysts to discuss FCX’s fourth-quarter and year-ended 2020 results is scheduled for today at 10:00 a.m. Eastern Time. The conference call will be broadcast on the Internet along with slides. Interested parties may listen to the conference call live and view the slides by accessing “fcx.com.” A replay of the webcast will be available through Friday, February 26, 2021.

FREEPORT: Foremost in Copper

FCX is a leading international mining company with headquarters in Phoenix, Arizona. FCX operates large, long-lived, geographically diverse assets with significant proven and probable reserves of copper, gold and molybdenum. FCX is one of the world’s largest publicly traded copper producers.

FCX’s portfolio of assets includes the Grasberg minerals district in Indonesia, one of the world’s largest copper and gold deposits; and significant mining operations in North America and South America, including the large-scale Morenci minerals district in Arizona and the Cerro Verde operation in Peru.

By supplying responsibly produced copper, FCX is proud to be a positive contributor to the world well beyond its operational boundaries. Additional information about FCX is available on FCX’s website at fcx.com.

Cautionary Statement and Regulation G Disclosure: This press release contains forward-looking statements in which FCX discusses its potential future performance. Forward-looking statements are all statements other than statements of historical facts, such as plans, projections, or expectations relating to ore grades and milling rates; business outlook; production and sales volumes; unit net cash costs; cash flows; capital expenditures; liquidity; operating costs; operating plans; FCX’s financial policy; FCX’s expectations regarding PT-FI’s ramp-up of underground mining activities and future cash flows through 2022; PT-FI’s development, financing, construction and completion of a new smelter in Indonesia and possible expansion of the smelter at PT Smelting; FCX’s commitments to deliver responsibly produced copper, including plans to implement and validate all of its operating sites under specific frameworks; improvements in operating procedures and technology; exploration efforts and results; development and production activities, rates and costs; tax rates; export quotas and duties; the impact of copper, gold and molybdenum price changes; the impact of deferred intercompany profits on earnings; mineralization and reserve estimates; execution of the settlement agreements associated with the Louisiana coastal erosion cases and talc-related litigation; and future dividend payments, share purchases and sales. The words “anticipates,” “may,” “can,” “plans,” “believes,” “estimates,” “expects,” “projects,” “targets,” “intends,” “likely,” “will,” “should,” “could,” “to be,” ”potential,” “assumptions,” “guidance,” “future” and any similar expressions are intended to identify those assertions as forward- looking statements. The declaration of future dividends is at the discretion of the Board and will depend on FCX’s financial results, cash requirements, future prospects, global economic conditions, and other factors deemed relevant by the Board. In accordance with the June 2020 amendment to the revolving credit facility, FCX is currently restricted from declaring or paying common stock dividends through December 31, 2021, unless FCX, at its option, reverts to the previous covenant requirements, which would also eliminate the restriction on the declaration or payment of common stock dividends.

FCX cautions readers that forward-looking statements are not guarantees of future performance and actual results may differ materially from those anticipated, expected, projected or assumed in the forward-looking statements. Important factors that can cause FCX’s actual results to differ materially from those anticipated in the forward-looking statements include, but are not limited to, changes in the credit ratings of FCX; changes in FCX’s cash requirements, financial position, financing plans or investment plans; changes in general market, economic, tax, regulatory or industry conditions; the duration and scope of and uncertainties associated with the COVID-19 pandemic, and the impact thereof on commodity prices, FCX’s business and the global economy and any related actions taken by governments and businesses; FCX’s ability to contain and mitigate the risk of spread or major outbreak of COVID-19 at its operating sites, including at PT-FI’s remote operating site in Papua; supply of and demand for, and prices of, copper, gold and molybdenum; mine sequencing; changes in mine plans or operational modifications, delays, deferrals or cancellations; production rates; timing of shipments; results of feasibility studies; potential inventory adjustments; potential impairment of long-lived mining assets; the potential effects of violence in Indonesia generally and in the province of Papua; the Indonesia government’s extension of PT-FI’s export license after March 15, 2021; risks associated with underground mining; satisfaction of requirements in accordance with PT-FI’s special mining license to extend mining rights from 2031 through 2041; the Indonesia government’s approval of a deferred schedule for completion of the new smelter in Indonesia; expected results from improvements in operating procedures and technology, including innovation initiatives; industry risks; regulatory changes; political and social risks; labor relations, including labor-related work stoppages; weather- and climate-related risks; environmental risks; litigation results; cybersecurity incidents; changes in general market, economic and industry conditions; financial condition of FCX’s customers, suppliers, vendors, partners and affiliates, particularly during weak economic conditions and extended periods of volatile commodity prices; reductions in liquidity and access to capital; FCX’s ability to comply with its responsible production commitments under specific frameworks and any changes to such frameworks; and other factors described in more detail under the heading “Risk Factors” in FCX’s Annual Report on Form 10-K for the year ended December 31, 2019, and Quarterly Reports on Form 10-Q for the quarters ended March 31, 2020, June 30, 2020, and September 30, 2020, each filed with the U.S. Securities and Exchange Commission (SEC), as updated by FCX’s subsequent filings with the SEC.

Investors are cautioned that many of the assumptions upon which FCX’s forward-looking statements are based are likely to change after the forward-looking statements are made, including for example commodity prices, which FCX cannot control, and production volumes and costs, some aspects of which FCX may not be able to control. Further, FCX may make changes to its business plans that could affect its results. FCX cautions investors that it does not intend to update forward-looking statements more frequently than quarterly notwithstanding any changes in its assumptions, changes in business plans, actual experience or other changes, and FCX undertakes no obligation to update any forward- looking statements.

This press release also includes forward-looking statements regarding mineralized material not included in proven and probable mineral reserves. Mineralized material is a mineralized body that has been delineated by appropriately spaced drilling and/or underground sampling to support the estimated tonnage and average metal grades. Such a deposit cannot qualify as recoverable proven and probable reserves until legal and economic feasibility are confirmed based upon a comprehensive evaluation of development costs, unit costs, grades, recoveries and other material factors. Accordingly, no assurance can be given that the estimated mineralized material not included in reserves will become proven and probable reserves.

This press release also contains certain financial measures such as adjusted net income and unit net cash costs per pound of copper and molybdenum, which are not recognized under U.S. generally accepted accounting principles. As required by SEC Regulation G, reconciliations of these measures to amounts reported in FCX’s consolidated financial statements are in the supplemental schedules of this press release.

Original Article: https://s22.q4cdn.com/529358580/files/doc_news/2021/FCX_4Q_2020_Earnings_Release.pdf